Freelance vs Salary Tax: Understanding Employer–Employee Relationship and Why Contract Income not equal to Salary

Understand freelance vs salary tax: why contract income is taxed as business/profession not salary, key judicial rulings, TDS & practical tax implications in India.

Table Of Content

- What this article is about?

- Why this matters

- Employer–Employee Relationship – Legal Tests & Indicators

- Freelance vs Salary Tax – Why freelancing/contract income is not equal to salary (tax & practical reasons)

- Judicial clarifications & landmark cases

- Practical differences – table: Salary vs Business/Professional Income

- For employers/clients – how to treat payments to freelancers

- Two examples – mini case studies

- Checklist – Are you an employee or a contractor?

- FAQs (short)

- Can a freelancer be treated as an employee?

- What TDS applies to contractor payments?

- Will I get Form 16 as a freelancer?

- Can an employer avoid PF by calling me a contractor?

- What deductions can freelancers claim?

- Conclusion

What this article is about?

If you’re a freelancer, contractor or a small business owner, freelance vs salary tax is the single most practical tax question you’ll face: am I an employee (salary rules) or an independent supplier (business/profession rules)? The answer changes how you’re taxed, what deductions you can claim, and whether your client must deduct TDS as salary or as contractor/professional fees.

Why this matters

Classifying income correctly matters for: TDS, filings (Form 16 vs Form 16A), deductions and bookkeeping, applicability of PF/ESI, GST, and legal protections. Courts and tribunals use multi-factor tests – not a single form or label – to decide if work is employment or contract. Below I unpack the legal tests, tax consequences, landmark rulings, practical checklists and examples you can use today.

Employer–Employee Relationship – Legal Tests & Indicators

Tax and labour courts don’t rely on one single factor. They apply several tests (the control test, integration/organisation test, mutuality of obligation and economic reality). The Supreme Court in recent judgments has reiterated a multi-factor, fact-driven approach rather than a single mechanical test.

Common indicators courts and tribunals look at:

- Control test: Does the payer control how the work is done (not just what)?

- Integration test: Is the worker integrated into the payer’s organisation (part of core operations) or externally separate?

- Mutuality of obligation: Is the client obliged to provide work, and the worker obliged to accept it?

- Ability to subcontract or hire helpers: Can the worker engage others? If yes, leans to contractor.

- Payment method: Salary (fixed periodic pay, benefits) vs invoices for completed projects.

- Provision of tools / workplace: Employer supplies tools/workplace (employee-like); contractor supplies own tools.

- Duration & exclusivity: Long-term single assignment with exclusivity looks like employment.

- Leave, notice, disciplinary control: Existence of leave rules, notice periods, disciplinary action points to employment.

These are indicators – the totality of facts decides the outcome (no single box checked makes the relationship one or the other).

Freelance vs Salary Tax – Why freelancing/contract income is not equal to salary (tax & practical reasons)

Legally, income gets taxed under different heads:

- Salaries (defined under the income-tax provisions) cover wages, allowances, perquisites and profits in lieu of salary; employers deduct TDS under salary rules and issue Form 16.

- Profits & gains of business or profession apply to freelancers, consultants and contractors; income is shown in business/profession schedules, requires books, and sometimes audit/advance tax obligations. The relevant tax heads and sections differ in substance and relief available. (Refer to the Income-Tax head definitions and the new Income Tax Act rules when relevant.)

Practical tax differences:

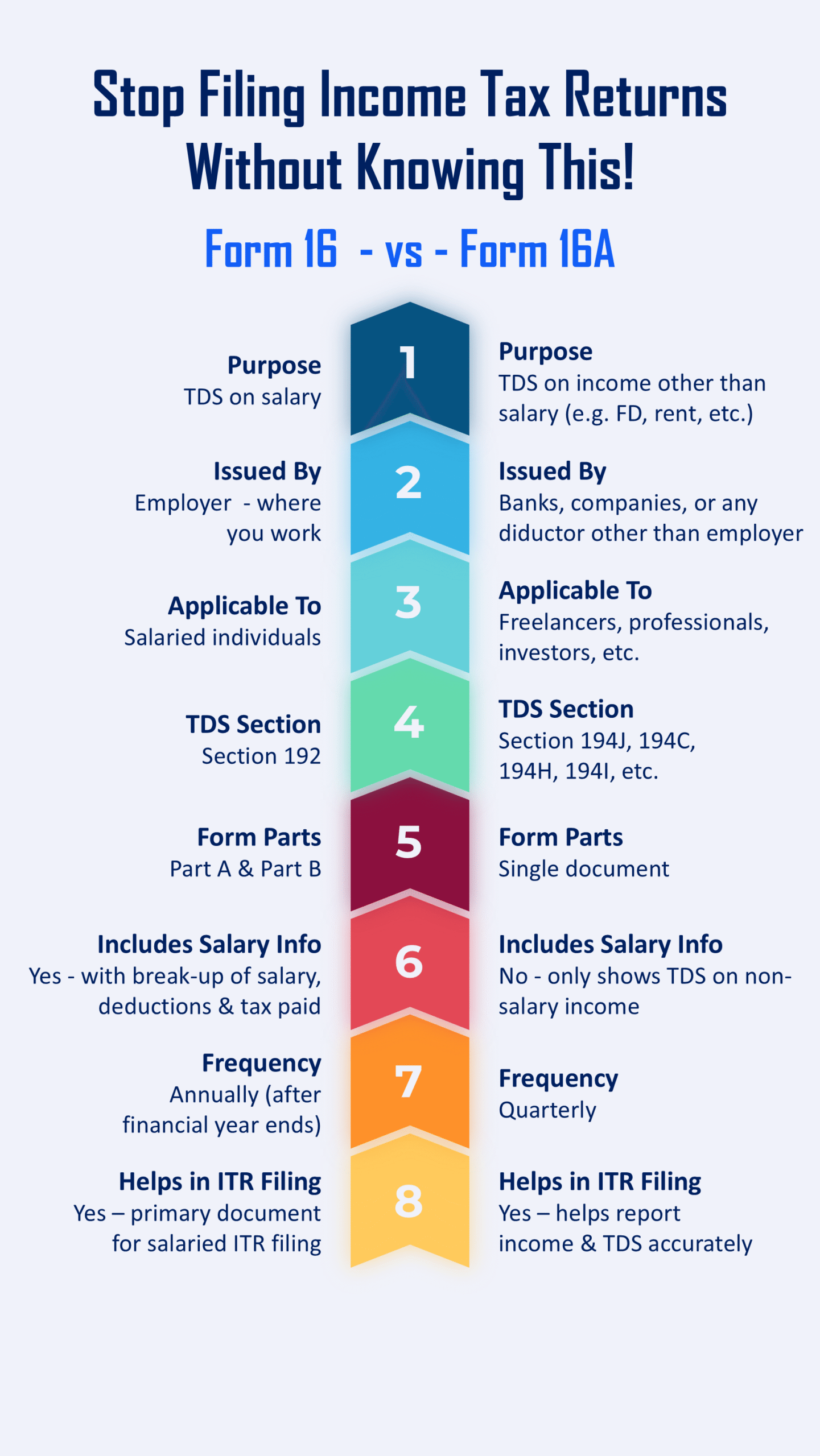

- TDS & certificates: Employers deduct TDS on salaries (Form 16). For contractors/freelancers the payer deducts under relevant sections (e.g., section 194C for contractors, section 194J for professional/technical fees) and issues Form 16A (TDS certificate for non-salary).

- Deductions: Salaried individuals get limited specific deductions (standard deduction, exemptions like HRA). Freelancers under business/profession can claim wider business expenses (office costs, depreciation, internet, telephone), subject to maintenance of books and audit rules.

- Advance tax: Freelancers generally must pay advance tax during the year if tax liability exceeds thresholds; salaried employees often meet tax via TDS by employer.

- GST: Many freelancers cross the GST registration threshold and must collect/comply with GST; employers paying salary are not involved in supplier GST treatment.

- Social security (PF/ESI): Applicable where employment exists; typically not for independent contractors.

Judicial clarifications & landmark cases

Below are authoritative decisions that lawyers and tax practitioners frequently cite when assessing whether work is employment or independent contracting. These are publicly verifiable judgements – read the full text at the linked sources.

- Sushilaben Indravadan Gandhi v. New India Assurance Co. Ltd. (Supreme Court, 15 Apr 2020) – Supreme Court revisited the contract of service vs contract for service distinction and reiterated the multi-factor approach (control, integration, remuneration method, economic reality). Useful when deciding whether a professional engaged under a contract is an employee. Indian Kanoon Supreme Today

- Balwant Rai Saluja v. Air India Ltd. (Supreme Court, 25 Aug 2014 – 9 SCC 407) – Court applied the integrated tests to decide whether canteen workers engaged through a contractor were employees of Air India. The judgment emphasises effective and absolute control as a key factor. Indian Kanoon

- Dharangadhara Chemical Works Ltd. v. State of Saurashtra (AIR 1957 SC 264) – early Supreme Court authority applying control/integration concepts to distinguish workmen/employees from independent operatives. Still cited for basic tests. Indian Kanoon

- V.D. Talwar v. CIT (Supreme Court, 1963) – classic tax decision holding that salary paid in lieu of notice is taxable as salary – important when characterising lump-sum payments by employers. Indian Kanoon

- Commissioner of Income Tax v. Kiranbhai H. Shelat (Gujarat High Court / Tribunals – 1998) – case where incentive/bonus was treated as salary rather than business/professional receipt shows how the nature of payment (tied to employment) determines the tax head. Indian Kanoon

Note: These cases are examples of judicial reasoning; the facts control the outcome. Always read the full judgment for granular tests and application.

Practical differences – table: Salary vs Business/Professional Income

| Feature | Salary | Business / Professional (Freelance) |

|---|---|---|

| Tax head | Salaries (salary rules, perquisites) | Profits & Gains of Business/Profession |

| Deductions | Limited (standard deduction, specified exemptions) | Broad business expenses (office, travel, depreciation) |

| TDS form | Form 16 (employer) | Form 16A (deductor) — TDS under 194C/194J etc. Income Tax India |

| Advance Tax | Usually covered by employer TDS | Assessee must compute & pay advance tax |

| PF/ESI | Employer applies (if employment) | Not applicable (unless misclassified) |

| GST | Not applicable on salary | May apply if services cross threshold |

| Audit | No special audit (salary returns) | Audit rules (section 44AB/limits) may apply |

For employers/clients – how to treat payments to freelancers

Best practices to avoid misclassification:

- Use clear contracts that describe deliverables, timelines and payment terms (avoid clauses that resemble an employment contract like fixed working hours, leave & discipline).

- Pay by invoices (with GST if applicable) and avoid salary-style payroll credit for contractors.

- Deduct correct TDS: section 194C for contractors (works contract), section 194J for professional fees.

- Issue Form 16A for TDS on contractor/professional payments, not Form 16 (salary).

- Avoid insistence on exclusivity or provision of tools/workplace that make the contractor appear integrated.

- Document the working relationship (SOW, delivery milestones, payment on invoice) and retain proofs showing independent nature of work.

Two examples – mini case studies

Case A – Software developer doing project-based gigs

Rohit develops mobile apps for 4 startups, invoices per project, uses his own laptop and timings, hires a designer when needed. Likely classification: contractor / professional. Tax: report under business/profession, claim expenses, manage advance tax; TDS likely under 194J (professional fees) if payer deducts.

Case B – Content writer engaged by single company long term

Neha writes daily content for one fintech company, follows editorial calendar, works fixed hours, receives monthly fixed payment and participates in performance reviews. Facts suggest employment (or at least close to it). Tax: income may be treated as salary; employer must deduct TDS on salary (Form 16) and statutory benefits may apply.

Checklist – Are you an employee or a contractor?

Score each item Yes = 1 / No = 0. If total ≥5, likely employee; ≤2, likely contractor; in-between = fact-dependent.

- Work supervised and controlled in manner of performance?

- Paid fixed periodic salary (not per invoice/project)?

- Provided company tools / workplace?

- Required to accept all tasks / exclusivity?

- Subject to company disciplinary rules?

- Entitled to paid leave / benefits?

- Company deducts TDS as salary & issues Form 16?

- Cannot sub-contract / delegate work?

FAQs (short)

Can a freelancer be treated as an employee?

Yes – if evidence shows employer-style control, integration, exclusivity and other employee indicia. Courts decide on facts.

What TDS applies to contractor payments?

Depends: section 194C for contractor payments (works), section 194J for professional/technical fees; see CBDT/Income Tax FAQs.

Will I get Form 16 as a freelancer?

Usually no. Form 16 is for salary. Freelancers receive Form 16A when TDS is deducted for non-salary payments.

Can an employer avoid PF by calling me a contractor?

Companies sometimes misuse contracts; courts look at substance over form. Misclassification risks employer liabilities and penalties. See Supreme Court tests.

What deductions can freelancers claim?

Freelancers can claim reasonable business expenses (home office, subscriptions, software, travel) subject to records and audit rules.

Pull-quote (highlighted): “Label is not destiny — the facts are. Courts look at how you work, not just what the contract says.”

Conclusion

If you’re unsure, consider a short consult with a CA or employment lawyer before you sign long-term contracts. Misclassification can cost both parties.

{kind=link}